Supermarket Competition Analysis: Australia vs New Zealand vs UK Executive Summary post

Anthonie Van Bosch

9/30/20256 min read

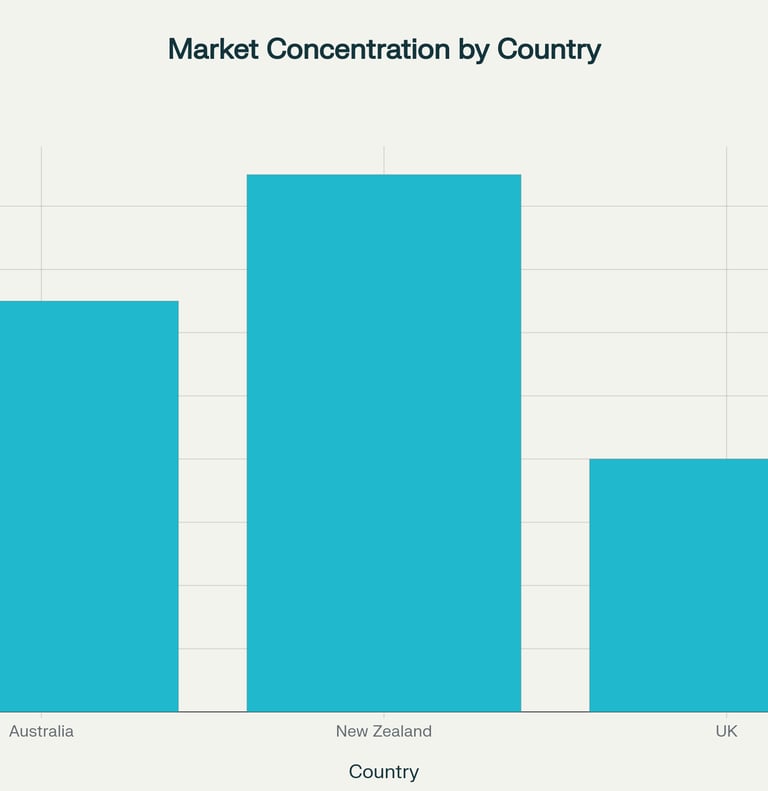

The investigation reveals stark differences in supermarket competition across the three countries, with New Zealand exhibiting the highest concentration and consumer harm, Australia facing an oligopoly with excessive profitability, and the UK maintaining the most competitive environment. New Zealand's virtual duopoly (85% market share) significantly exceeds Australia's concentrated duopoly (65%) and the UK's more competitive oligopoly (40% for top two players).

Market concentration comparison showing the combined market share of the top two supermarket players in Australia (65%), New Zealand (85%), and the UK (40%)

Market Structure and Concentration

New Zealand: Extreme Duopoly

New Zealand operates under a virtual duopoly between Foodstuffs (53% market share) and Woolworths (32.4% market share), collectively controlling 85-90% of the market. This represents one of the most concentrated grocery markets globally, with the Commerce Commission estimating a Herfindahl-Hirschman Index (HHI) of 3,601 in 2024, indicating extremely high concentration.

Australia: Dominant Duopoly

Australia's market is dominated by Woolworths (38% market share) and Coles (29% market share), together holding approximately 65-67% of the market. The addition of Aldi (9%) and Metcash/IGA (7%) brings the top four players to over 80% market control.

United Kingdom: Competitive Oligopoly

The UK maintains a more competitive structure with Tesco (28.4% market share), Sainsbury's (16%), Asda (13.4%), and Morrisons forming the "Big Four". The combined market share of the top two players is approximately 40%, significantly lower than Australia and New Zealand.

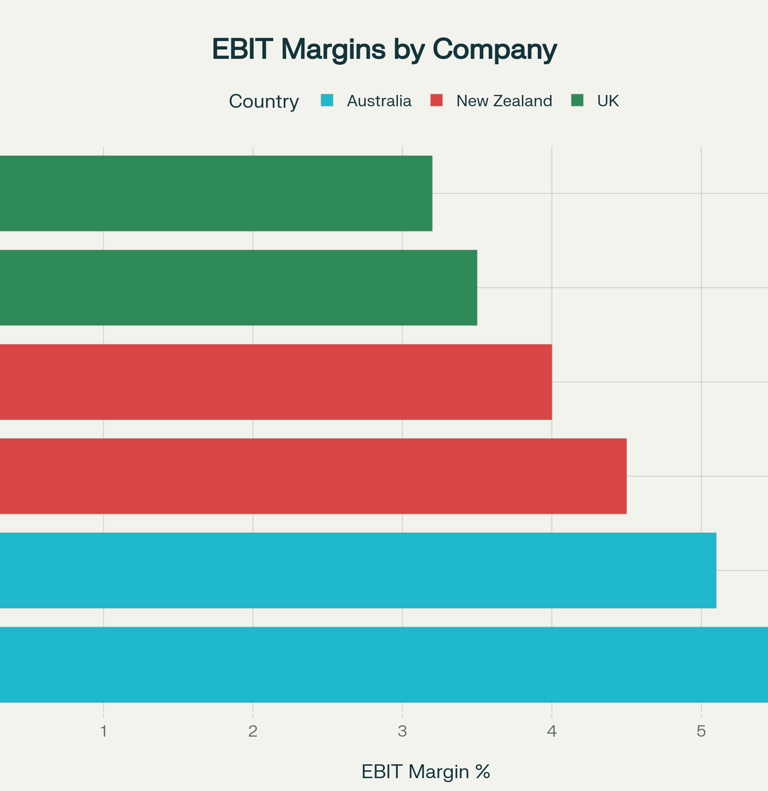

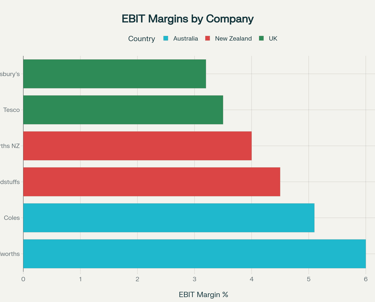

EBIT profit margins comparison across major supermarket chains in Australia, New Zealand, and the UK, showing Australian supermarkets achieving the highest profitability

Profitability and Pricing Analysis

Excessive Profit Margins

Australian supermarkets demonstrate the highest profitability globally, with EBIT margins of 5-6% for Woolworths and Coles, compared to 2-4% for UK supermarkets like Tesco and Sainsbury's. The ACCC found that "ALDI's, Coles' and Woolworths' EBIT margins are among the highest of supermarket businesses in relevant comparator countries".

New Zealand supermarkets maintain EBIT margins of 4-5%, while earning an estimated $430 million annually in excess profits between 2015-2019 due to limited competition.

Price Comparisons

Despite claims of competitive pricing, international comparisons reveal significant price variations. A standardized basket comparison shows:

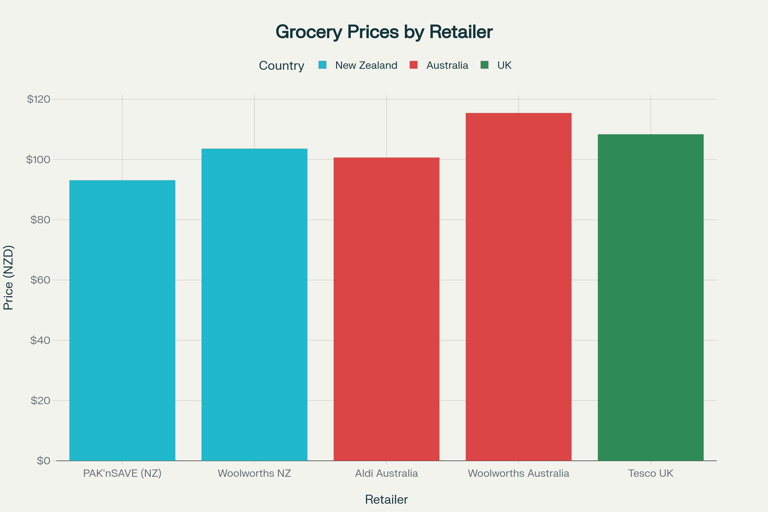

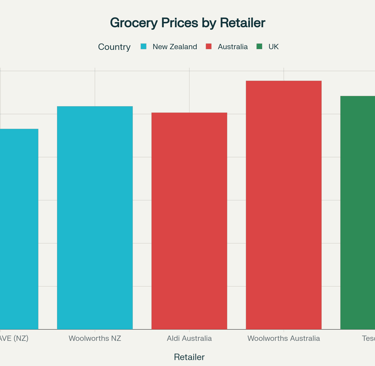

Grocery basket price comparison across retailers in Australia, New Zealand, and UK (in NZD), showing PAK'nSAVE as the most affordable option

Key finding: New Zealand's PAK'nSAVE offers the lowest prices at NZD $93.09, while Australian Woolworths charges the highest at NZD $115.44. However, these comparisons must account for GST differences, as New Zealand applies 15% GST to all food items while Australia exempts basic groceries and the UK has no VAT on most food products.

Regulatory Response and Reform Strategies

Australia: Competition Law Enhancement

Australia is implementing comprehensive merger reform with mandatory merger notifications from January 1, 2026. The approach focuses on:

Strengthening competition law with enhanced merger control and prohibition of excessive pricing

Mandating price transparency through APIs and price monitoring systems

ACCC inquiry powers with increased funding of over $30 million for enforcement

Designated transaction requirements specifically targeting supermarket acquisitions

New Zealand: Structural Intervention

New Zealand is pursuing the most aggressive reform approach, actively considering structural separation and divestment powers. The government has commissioned specialist advice on:

Potential de-merger of existing brands to create genuine competition

Structural separation of existing entities to fundamentally alter market dynamics

Enhanced wholesale regulation with penalties up to $10 million for breaches

Grocery Supply Code strengthening to address supplier-retailer power imbalances

Commerce and Consumer Affairs Minister Andrew Bayly stated: "If legislation is needed, I would want to introduce it before the end of the year and pass it during this parliamentary term, with rapid implementation shortly thereafter".

United Kingdom: Market-Based Approach

The UK maintains minimal regulatory intervention, relying on market-based competition and existing competition law. The Competition and Markets Authority (CMA) provides monitoring rather than structural intervention, reflecting the more competitive market environment.

Geographic and Access Inequities

New Zealand's Regional Monopolies

The Commerce Commission identified significant geographic inequities, with consumers in Auckland enjoying more competition (71% major supermarket share) compared to rural areas where supermarkets function as localized monopolies (88% market share outside main cities). Some rural areas have "minimal to no choice within their locality".

Australia's Widespread Reach

Australia maintains more consistent access, with both Woolworths and Coles operating extensive national networks. However, the duopoly structure limits genuine price competition across all regions.

UK's Diverse Competition

The UK benefits from diverse regional competition, with discount retailers like Aldi and Lidl gaining market share (Aldi reached 11.2% market share in 2025), providing genuine alternatives across different geographic areas.

Consumer Impact and Economic Consequences

Price Inflation Patterns

New Zealand recorded 1.2% annual food price inflation in September 2024, with Foodstuffs co-ops achieving 0.0% inflation for comparable baskets. However, grocery prices remain 3% above OECD average despite recent stabilization.

Australia experienced higher food price inflation of 3.4% annually, while the UK recorded 1.3%. The OECD noted that New Zealand's poor productivity rankings are partially attributable to "broken markets in sectors like banking and groceries, which make excess profits".

Consumer Behavior Changes

High grocery prices are driving significant behavioral changes:

69% of New Zealand shoppers now compare prices between supermarkets

Consumers increasingly shop at discount retailers and buy promotional items

PAK'nSAVE's market share growth reflects consumer price sensitivity

The Way Forward: Critical Reform Pathways

Australia's Comprehensive Legal Framework

Australia's reform strategy emphasizes strengthening existing competition mechanisms rather than structural breakup. The new mandatory merger regime specifically targets supermarket acquisitions, requiring ACCC notification for any supermarket transaction. This approach aims to prevent further concentration while enhancing price transparency through mandatory unit pricing and promotional disclosure requirements.

New Zealand's Structural Revolution

New Zealand is pursuing the most radical structural intervention, with potential legislation for mandatory divestment by late 2025. The approach recognizes that regulatory measures alone cannot address the fundamental market structure problems. As noted in legal analysis, divestiture would likely be favored by courts given the extreme concentration and lack of viable alternatives.

Effectiveness Assessment

The UK's competitive market structure demonstrates that lower concentration naturally results in better consumer outcomes without requiring extensive regulatory intervention. UK supermarkets operate with profit margins of 2-4% compared to 5-6% in Australia and 4-5% in New Zealand, directly benefiting consumers through lower prices and better service.

Conclusion

The UK emerges as the clear winner in supermarket competition, offering the lowest concentration (40% for top two players), most competitive pricing relative to income levels, and minimal need for regulatory intervention. New Zealand faces the most severe competition problems with its 85% duopoly requiring urgent structural intervention, while Australia occupies a middle position with high profitability concerns but more regulatory options for reform.

The evidence strongly suggests that market concentration directly correlates with consumer harm. New Zealand's consideration of divestment powers represents the most appropriate response to extreme market concentration, while Australia's enhanced competition law approach may prove sufficient for its less concentrated market. The UK's experience demonstrates that competitive markets can function effectively with minimal regulatory intervention when structural competition exists.

Success in grocery competition reform ultimately depends on creating genuine competitive tension—whether through the threat of divestment in New Zealand, enhanced merger control in Australia, or maintaining the competitive structure that already exists in the UK.

https://www.gourmetpro.co/blog/biggest-supermarkets-australia

https://www.statista.com/topics/8773/sainsbury-group-in-the-united-kingdom-uk/

https://www.equaljusticeproject.co.nz/articles/supermarket-duopoly-a-hunger-for-change2023

https://www.statista.com/topics/6399/supermarkets-and-grocery-retail-in-australia/

https://www.statista.com/statistics/280208/grocery-market-share-in-the-united-kingdom-uk/

https://uk.finance.yahoo.com/news/tesco-not-losing-grip-uk-104557136.html

https://www.accc.gov.au/system/files/supermarkets-inquiry_1.pdf

https://www.foodstuffs.co.nz/news-room/2025/PAKnSAVE-tops-international-grocery-price-comparison

https://www.landers.com.au/legal-insights-news/new-era-for-merger-control-in-australia

https://colemangreig.com.au/insights/publications/australias-new-merger-laws-from-1-july-2025/

https://www.beehive.govt.nz/speech/delivering-better-grocery-prices

https://ojs.victoria.ac.nz/vuwlr/article/download/9801/8623/16059

https://www.linkedin.com/pulse/uk-grocery-market-comparative-analysis-tesco-cem-buyukkaya-vuzwe

https://www.morningstar.com.au/stocks/this-household-asx-name-just-got-moat-upgrade

https://www.linkedin.com/pulse/numbers-oecd-grocery-prices-chris-quin-kq1vc

https://www.ernienewman.com/single-post/oecd-tables-possible-nz-supermarket-breakup

https://www.statista.com/statistics/1453348/australia-woolworths-supermarkets-by-state/

https://www.treasury.govt.nz/sites/default/files/2022-02/oia-20210006.pdf

https://www.ibisworld.com/australia/industry/supermarkets-and-grocery-stores/1834/

https://www.onefarm.co.nz/blog/an-answer-to-nzs-supermarket-duopoly

https://market.worldpanelbynumerator.com/en/grocery-market-share/great-britain

https://www.consumer.org.nz/articles/how-we-got-a-supermarket-duopoly

https://en.wikipedia.org/wiki/List_of_supermarket_chains_in_the_United_Kingdom

https://teachin.com.au/cost-of-living-in-the-uk-vs-australia--nz-and-canada/

https://www.hsfkramer.com/insights/2024-10/australian-government-introduces-merger-reform-bill

https://www.consumer.org.nz/articles/what-s-the-cheapest-supermarket

https://www.corrs.com.au/insights/the-new-accc-merger-regime-a-round-up-of-recent-announcements

https://www.consumer.org.nz/articles/australia-vs-nz-supermarket-competition-compared

https://www.accc.gov.au/inquiries-and-consultations/supermarkets-inquiry-2024-25

https://www.linkedin.com/pulse/facts-our-international-grocery-price-comparison-chris-quin-nmxkc

https://www.australiancompetitionlaw.info/reports/database/2024-2025-supermarket-inquiry

https://supermarketnews.co.nz/global/accc-releases-guidance-on-merger-reform-transition/

https://fisherfunds.co.nz/news-and-insights/supermarkets-dodge-governments-hospital-pass

https://www.accc.gov.au/business/mergers-and-acquisitions/merger-reform

https://www.accc.gov.au/business/mergers-and-acquisitions/merger-control-regime